Imagine this: You meet with your accountant at the end of the year to review your tax return and she tells you fantastic news. You made a sizable profit in your business! But you’re stunned because there’s no cash in the bank and you have no idea how you’re going to pay the income taxes now due on the profit.

How can this possibly happen? How can a business turn a profit yet not have any cash at the end of the year to show for it? Believe it or not, this is more common than you think. In fact, it has probably happened to you or someone you know and it can be surprising, to say the least.

Not All Cash Transactions Are Income or Expenses

Cash flow is exactly how it sounds—the way cash flows through a business as deposits and withdrawals. The profit of a business is the difference between the gross income or sales of a business and its expenses.

A company can have positive cash flow while having no profit if the cash comes from sources other than income, such as when an owner puts in their own money or if they take out a loan. These types of transactions aren’t income but rather liability or equity transactions that appear on the balance sheet.

Conversely, a company can have negative cash flow while having a large profit if the owners take cash out of the business to pay personal expenses or use it to make investments or loans to others. These types of cash out transactions are also reported on the balance sheet, not the profit and loss statement.

The difference between cash flow and profit really comes down to the source of cash transactions and the accounting basis.

What Is Accounting Basis?

While the source determines whether the transaction is categorized as income or an expense, the accounting basis determines when you report income and expenses, and greatly affects the amount of profit you report for a period. There are two general methods of accounting:

- Accrual basis accounting means that you recognize your income and expenses when you earn or incur them.

- Cash basis accounting means that you recognize the income and expenses when cash is exchanged (hence the name).

Many business owners use the balance in their bank account to gauge the profitability of their business. But this can be a big problem if your company extends credit to your customers or uses credit to finance your purchases because those transactions won’t be reflected in the bank account activity until they are paid.

If your company transacts using credit, you likely use a spreadsheet or double-entry accounting system (like QuickBooks) to keep track of what your customers owe you and how much you owe to your vendors. These invoices and bills are recorded in the accounts receivable and accounts payable ledgers, respectively. As you receive or make payments, you mark the invoices and bills as paid in the ledgers and reduce the balances. Accounts receivable and accounts payable are both reported on the balance sheet. Check out this article to learn more about the balance sheet.

How Does Accounting Basis Affect Your Bottom Line?

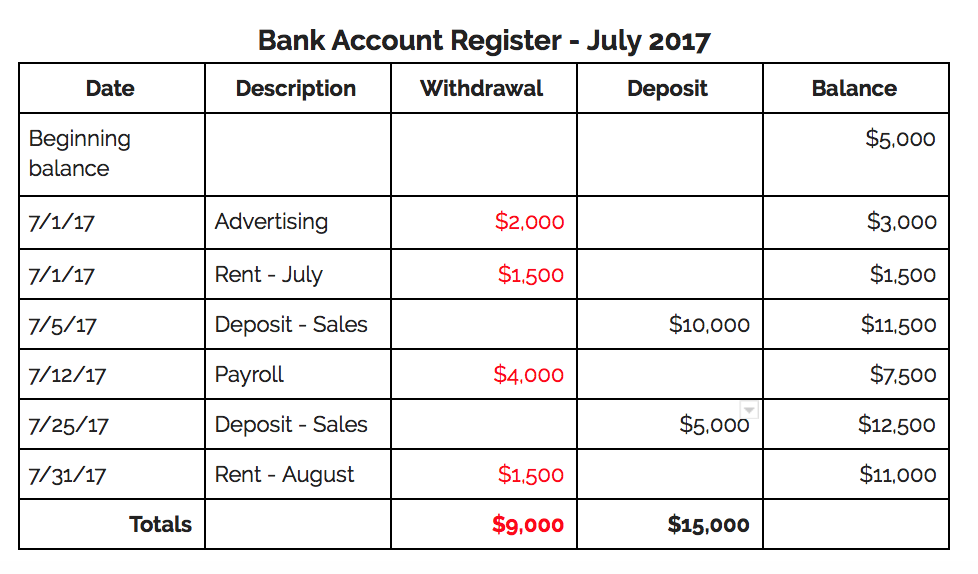

Let’s take a look at an example to illustrate how the accounting basis of transactions could affect your profit for a period. In our example, your business account shows the following checks and deposits for the period of July:

We can see that the company deposited $6,000 more into the bank account than it spent for the month, which increased the cash balance to $11,000. Looks like you had a very good month!

We can see that the company deposited $6,000 more into the bank account than it spent for the month, which increased the cash balance to $11,000. Looks like you had a very good month!

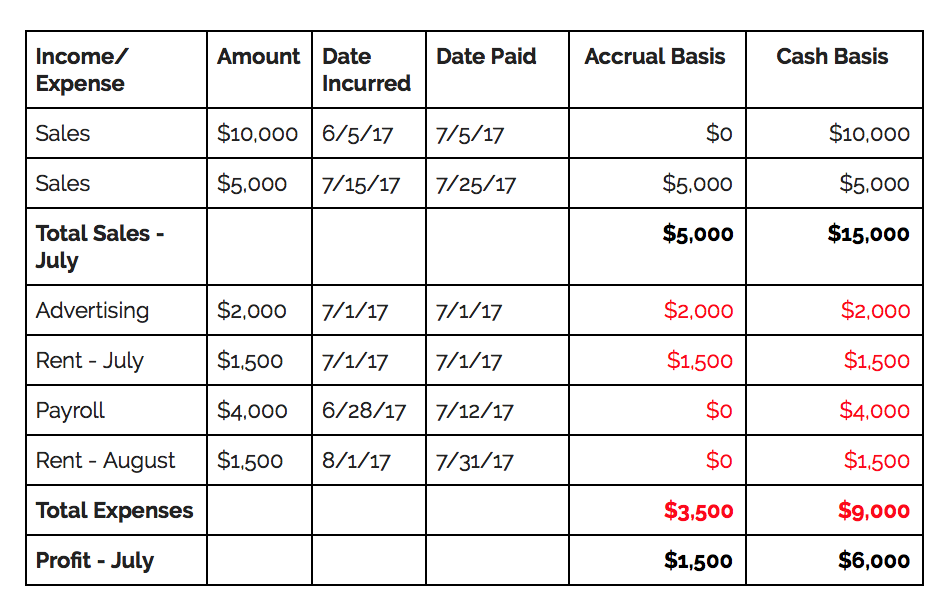

Now, let’s take a look at how these transactions are reported on both a cash and accrual basis:

Notice that the profit on an accrual basis is significantly lower than the cash basis profit! Let’s take a look at the differences and how the profit could be so different:

Notice that the profit on an accrual basis is significantly lower than the cash basis profit! Let’s take a look at the differences and how the profit could be so different:

- The $10,000 deposit on July 5th was actually payment for a sale that occurred in June and would have been included on the June profit and loss statement.

- The same is true for the payroll paid on July 12th that was for the pay period ending June 28th.

- The rent payment made on July 31st isn’t included on the profit and loss statement for July because it is a prepayment of the August rent and will be included in the August profit and loss statement.

You can see how the accounting basis can really make a difference in the reported bottom line of a business and its profit. It’s important to know whether your business reports its income to the IRS on a cash or an accrual basis on your tax return. If you run your business on a cash basis but report to the IRS on an accrual basis, you can bet there will be differences. Make sure you know what to expect by working with a qualified tax professional.

The post Cash Flow vs. Profit: What’s the Difference? appeared first on Fundera Ledger.

from Fundera Ledger https://www.fundera.com/blog/cash-flow-vs-profit

No comments:

Post a Comment