What Is Business Bankruptcy?

If you’re struggling to pay off business debts, filing for business bankruptcy might help. Business owners can file for Chapter 7, Chapter 11, or Chapter 13 bankruptcy, depending on the business’s debt levels and financial situation. A Chapter 7 filing typically ends in the liquidation of the business, with the assets distributed among creditors. A Chapter 11 or Chapter 13 filing usually ends in the reorganization of the business’s debts, but the company can continue operating.

When it comes to the future of your business, filing for business bankruptcy might seem like the worst thing that could happen. You might feel like your business is failing, and you might be worried about how filing for bankruptcy will affect your credit score or your access to financing in the future.

Bankruptcy is designed to help struggling businesses eliminate or repay their debt. There are some serious consequences of filing for bankruptcy, and you should never make the decision to file lightly. That said, having to file for business bankruptcy is not necessarily a death sentence—in fact, it could mean the difference between your business sinking or surviving. Indeed, some business owners even file for bankruptcy strategically, as a way to streamline their debt and get a fresh start.

The process of filing for bankruptcy and the results vary depending on the type of bankruptcy. Business owners can file for Chapter 7, Chapter 11, or Chapter 13 bankruptcy, depending on their financial situation and on the type of company that they have. As a business owner, you need to carefully consider which chapter you file under, the consequences and opportunities of filing, and the cost and time involved in filing. Let’s review these issues, so you can understand what happens when your business files for bankruptcy.

The 3 Types of Business Bankruptcy and What Happens in Each Case

Small business owners have three basic options if they need to file for business bankruptcy: Chapter 7, Chapter 11, or Chapter 13. In each case, the process and result are a little different. Here’s an overview of the three types of business bankruptcy and what happens in each case.

Chapter 7 Bankruptcy (Liquidation)

Chapter 7 bankruptcy is the most common type of bankruptcy, making up about 80% of filings. Chapter 7 bankruptcy is available to consumers and all types of businesses. This is an option if you do not have a means to keep your business running, and are unable to pay off your company’s current debts. The result of a Chapter 7 business bankruptcy filing is liquidation of the business’s assets and closure of the business.

Linda Worton Jackson, a partner at commercial law firm Pardon, Jackson, Gainsburg, PL explains, “Once a business files for Chapter 7, the company shuts down, the officers, directors, and employees are dismissed, and a court appointed trustee takes over to liquidate the company for the benefit of creditors. The company does not continue operating under Chapter 7, except in very rare circumstances where the trustee allows it to do so temporarily.”

Consumer who file for Chapter 7 bankruptcy need to show that their income is low enough to qualify. Filers who are seeking to discharge business debts do not need to meet income requirements. If you have multiple creditors who you haven’t paid back, the trustee will divide up your assets among those creditors. Certain assets that fall under bankruptcy exemption laws are safe from creditors. For instance, most states and the federal bankruptcy laws provide some protection for a filer’s home.

Corporations, limited liability companies, partnerships, and sole proprietorships are all eligible to file Chapter 7, but it’s mostly a tool used by sole proprietors. Once the creditors get paid, and the trustee receives their fee, sole proprietors receive a discharge. A discharge means that you’re no longer responsible for paying back business debt, even if you signed a personal guarantee. Corporations, LLCs, and partnerships can’t receive formal discharges, so if you’ve signed a personal guarantee on a loan, creditors can still come after your personal assets to satisfy a debt.

Chapter 11 Bankruptcy (Reorganization)

Chapter 11 bankruptcy allows a business to continue operating while reorganizing debts. Businesses pursue this option when they’re not completely under water and have the potential to continue operating as a viable company with some help from the bankruptcy court.

Jackson says, “In a Chapter 11 bankruptcy, the management remains in control, and has the ability to make decisions for the company, with the court’s approval. When a company reorganizes, it means it will emerge from bankruptcy as an operating company as opposed to liquidation. The business will use the bankruptcy process to eliminate debt, sell off non-performing assets, restructure long-term debts, and possibly bring in new equity or financing.”

In order to be eligible for a Chapter 11 filing, your company must be generating regular revenues. If you go this route, you’ll have to submit a reorganization plan to the court showing how and when you expect to repay all your debts. Your creditors and the court must review and approve the plan before it goes into effect.

Chapter 11 bankruptcy essentially allows you to negotiate with your creditors. For instance, instead of having to pay back your loan within five years, the court might allow you to make payments over the next 20 years. The goal of a Chapter 11 bankruptcy is to make sure you can continue operating, by balancing expenses and income and helping you regain profitability over an extended period of time.

Chapter 13 Bankruptcy (Reorganization)

Chapter 13 bankruptcy is an option that’s primarily for consumers, but sole proprietors can use it as well. As Jackson explains, “Chapter 13 bankruptcy is very similar to Chapter 11, but is only applicable to small businesses with a few creditors… It is a simplified and less costly reorganization for small businesses.”

There are debt limits that determine eligibility for Chapter 13 bankruptcy. You can’t have more than $394,725 of unsecured loans or $1,184,200 of secured loans to qualify. These numbers change periodically to reflect inflation and cost of living changes.

Under Chapter 13, a sole proprietor can file for personal bankruptcy and petition the court to reorganize their debts. The key thing to remember is that as a sole proprietor, you have to file for bankruptcy under your own name, not the business’s name. Both personal and business debts come under the trustee’s purview. The trustee will treat your personal and business property in the same way—both are available to pay back all debt, business or personal.

With this type of bankruptcy, the business can continue operating. As with Chapter 11, you must submit a reorganization plan to the court for approval, showing how and when you plan to repay your debt. Depending on your income, personal and business expenses, and types of debt you have, you’ll either have to repay some or all of your outstanding debt (some might be discharged). Usually, under Chapter 13, you get 3 to 5 years to pay back the debt, so this is really only an option for businesses that have a small amount of debt. Businesses with a larger debt loan should consider Chapter 11 bankruptcy.

The Bankruptcy Process

Thinking through the pros and cons of bankruptcy and deciding if it is the right option for you is something that you must give careful thought and consideration to. Once you decide you want to proceed with bankruptcy, initiating the process is pretty simple. Sole proprietors can file on their own, but businesses need an attorney to file. And even if you’re a sole proprietor, we recommend hiring an attorney to get you through what can be a long, complicated process.

“The commencement of a bankruptcy is actually simple,” Jackson says, “with a form that must be filed, along with payment of a filing fee. But, after the case is opened, the company must file very extensive disclosures with the court. After that, management must become accustomed to making its secrets public and seeking approval of every move.” Bankruptcy is regulated by the U.S. Bankruptcy Court, of which there are 94 jurisdictions. You start you case by filing an official bankruptcy petition in the jurisdiction where your principal place of business is located.

After you file the initial petition, there’s a lot more paperwork that follows. Each type of bankruptcy has its own forms, and the forms vary for sole proprietors and registered business entities. For reorganization bankruptcies—Chapter 11 and 13—you must formally disclose your payment plan with the bankruptcy court, explaining how you plan to pay back your creditors and over what period of time. Your forms will also include information on your company’s business affairs, liabilities, and assets.

Creditors must approve your reorganization statement. This is because creditors need to be able to make an educated decision regarding your proposed plan. A confirmation hearing will take place next, where your plan for reorganization will be up for discussion. The bankruptcy court will either confirm or reject the plan. If confirmed, you can continue running the business in order to pay back your creditors. Most courts require updated financials from your business on a periodic basis, to make sure you’re complying with the reorganization plan.

Keep in mind that bankruptcy forms are public record, so creditors, other businesses, and curious friends or family members can look up your financial information in court.

How Long Does the Bankruptcy Process Take?

The entire bankruptcy process can take a long time and cost you a significant amount of money. A Chapter 7 bankruptcy usually winds up with a discharge within four to six months. A Chapter 13 bankruptcy takes a similar amount of time, though the actual period for paying back the debt is three to five years.

A Chapter 11 bankruptcy takes the longest amount of time. Creditors are allowed to question the debtor in court, and both creditors and the court need to review and approve the reorganization plan. All told, this can take upward of a year. If you’re using an attorney, the legal fees can really add up during the entire process.

Post-Bankruptcy: Will Your Credit or Access to Future Financing Be Affected?

What most people worry about after a bankruptcy is how it will affect their credit. When business owners file for bankruptcy, not only can their personal credit rating be affected. Their business credit score can also take a hit. Plus, your ability to access credit for your business in the future can be affected.

Bankruptcy’s Impact on Credit

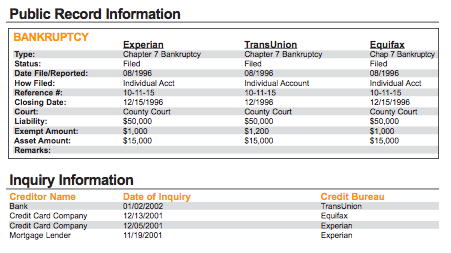

The impact to your credit from a bankruptcy depends on the type of business you have. If you are a sole proprietor, there’s no legal separation between you and your business. You are personally responsible for personal and business debts. When you file for bankruptcy, the court can discharge your debts. That means you no longer have to pay them back, but you’ll pay the price with a huge hit to your credit. Bankruptcies show up on your credit report for seven to 10 years and can damage your score by more than 130 points.

If you have a registered business entity, such as an LLC or corporation, then there’s a legal wall between you and the business. You’re not personally responsible for your company’s debts. In this case, neither the unpaid business debts nor the business bankruptcy should show up on your personal credit report. But, they will show up on your company’s commercial credit report. Lenders, the SBA, and suppliers check your business credit report to determine whether to do business with you.

The exception here—and this is a big exception—is if you’ve signed a personal guarantee. A personal guarantee makes you personally responsible for business debts, no matter how your business is structured. For example, even if you have a corporation, signing a personal guarantee makes you personally responsible for the corporation’s debts. In this case, the company’s creditors can come after your personal assets to satisfy the business debt, even if your business has filed for bankruptcy. And the unpaid debt will show up on your personal credit report.

Bankruptcy’s Impact on Your Access to Financing

Having a bankruptcy on your record can seriously limit your access to financing in the future. All lenders are concerned with one thing—getting paid back, with interest and on time. A bankruptcy in your record can make lenders wary of working with you, even if you’re seeking funding for a brand new company (after the former company was dissolved).

“Most lenders require you to wait for three to seven years after a completed bankruptcy until they’ll consider you for a business loan,” says Matthew Nicolosi, a senior sales manager at Fundera.

In the meantime, however, you are not completely without options. For instance, you can still apply for a business credit card, and some alternative lenders like Kabbage will work with you just one year after a bankruptcy discharge. Self-secured loans such as equipment loans are also a possibility, even with a recent bankruptcy.

Fundera’s Nicolosi advises small business owners to stay focused on improving their credit to open up access to financing in the future:

“After a bankruptcy, the best thing a borrower can do is stay hyper-focused on their credit profile. Obtain a business credit card or two to build up business and personal credit, minimize credit utilization to keep your scores maximized on that front, and ensure you’re keeping your business financials up to par with what the lenders are looking for so when the time does pass, you can pounce on those opportunities.”

A bankruptcy is an obstacle on your road to business funding, but it doesn’t have to completely shut you off from accessing the money you need to get your business back on track or launch a new business.

Drawbacks and Benefits of Filing for Bankruptcy

Filing for business bankruptcy is a last resort step for any company. You should consider filing for bankruptcy only if you are having serious trouble paying your debts, are tied up in litigation with creditors, or feel like your business is hanging on by a thread. The bankruptcy process can bring some structure to your finances and help you get through to the other side. However, if your business is really underwater, the bankruptcy process might mean that your business has to be dissolved.

Of course, it’s never a good idea to make a hasty decision to file for business bankruptcy—it will stay on your credit history for seven to 10 years and affect your access to financing. Be sure to explore all your options and talk with a lawyer before deciding what to do with your business in the near future.

The post What Happens When You File for Business Bankruptcy? appeared first on Fundera Ledger.

from Fundera Ledger https://www.fundera.com/blog/bankruptcy/

No comments:

Post a Comment